DirecTV LatAm bets on Amazon LEO satellites to offset pay-TV collapse

DirecTV Latin America is experiencing a significant decline in its pay-TV and DTH subscriber base, prompting a strategic shift towards OTT platforms and new infrastructure. The company is actively pursuing diversified strategies including partnerships with local ISPs, leasing neutral fiber networks (DFibra), M&A of fiber ISPs (ZAAZ), and an exclusive alliance with Amazon Kuiper for LEO satellite services starting in 2026. This complex transition aims to build the necessary scale and connectivity for its digital streaming future as its legacy DTH infrastructure approaches end-of-life.

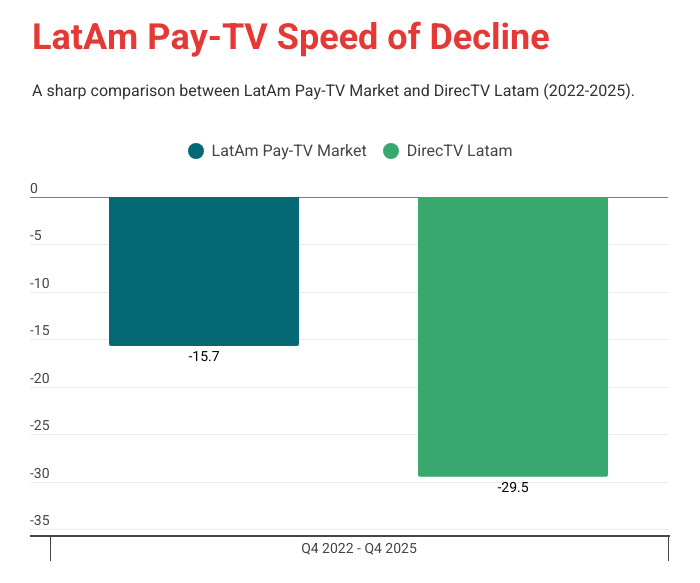

Key Takeaways

- Legacy DTH infrastructure is projected to reach technical expiration by 2031-2032 due to satellite lifespan limits.

- DirecTV's pay-TV contraction rate of 29.5% is nearly double the Latin American regional average of 15.7%.

- Commercial conversion on neutral networks lagged technical reach, totaling just 200,000 active accesses from a 40M homes-passed footprint.

- The 2026 Amazon Kuiper (now Amazon LEO) partnership provides an exclusive window for suburban and rural scale.

- Inorganic growth via ZAAZ acquisitions and a Brazilian MVNO launch represent the most capital-intensive pathway to immediate volume.

Why It Matters

DirecTV Latin America is racing against a literal technical countdown to migrate 60% of its base from aging DTH satellites to OTT-driven digital platforms. This transition is hampered by a 'scale dilemma' where digital growth cannot yet offset the legacy decline. By partnering with Amazon’s LEO constellation, the company bypasses the high costs and slow rollout of terrestrial fiber in rural markets, though it must contend with Starlink's established regional lead. The company's survival hinges on converting its legacy scale into a high-bandwidth ecosystem before its hardware expires. Watch the 2026 commercial rollout of Amazon LEO as the definitive signal for DirecTV's long-term viability in suburban and rural South America.

Additional Context

The strategic urgency at DirecTV Latin America, managed by parent Vrio Corp under the Werthein Group, aligns with broader regional shifts toward digital-first distribution. Per Reuters (June 2026), DirecTV recently struck a multi-year deal with sports streamer DAZN to carry DSPORTS channels across five Latin American countries, specifically for the 2026 FIFA World Cup. This commercial partnership highlights the shift toward content sub-licensing as a means to maintain relevance during the digital transition, especially as major rivals like Disney and Netflix have consolidated their regional presence through ad-supported tiers and bundled offerings. Direct competition in the connectivity space is also intensifying. While DirecTV leans on the 2026 commercial availability of Amazon LEO (formerly Project Kuiper), Starlink has already secured a significant lead. Per The Next Web (June 2026), Starlink's subscriber base more than doubled over the past year to 10.3 million users globally, with an aggressive expansion into price-sensitive markets like Brazil and Argentina. This first-mover advantage and the recent SpaceX IPO (June 2026), which valued the company at nearly $1.8 trillion, place immense pressure on DirecTV and Amazon to deliver gigabit speeds and localized support to differentiate their service. Further compounding the pressure is the broader decline of the traditional pay-TV revenue pool. According to 3vision (February 2026), regional pay-TV revenues are expected to fall from $13 billion in 2023 to roughly $9 billion by 2030. While digital OTT revenues in Latin America are forecast to climb to nearly $19 billion in that same period, the market is shifting from household penetration to density, where consumers layer multiple streaming services. For DirecTV, this means the battle is no longer just for the primary screen, but for the fundamental broadband connection that powers the entire household's digital stack.

Read full article at dataxis.com